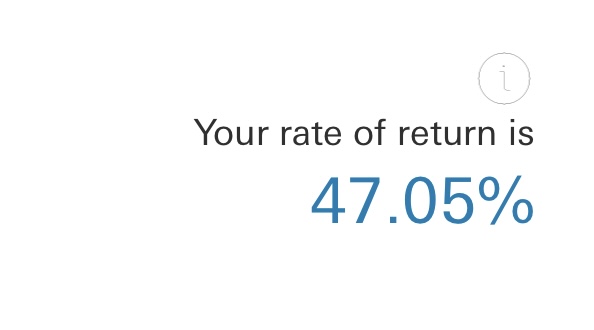

From May 2023 to today:JackyJoll wrote: Mon Oct 06, 2025 3:12 pm I can’t tell you anything really but I’m not sorry I put mine in an all equities Stocks & Shares ISA.

At least not sorry yet anyway!

From May 2023 to today:JackyJoll wrote: Mon Oct 06, 2025 3:12 pm I can’t tell you anything really but I’m not sorry I put mine in an all equities Stocks & Shares ISA.

At least not sorry yet anyway!

Git. Mine's half that. I'm going to be working till I'm 80weeksy wrote: Mon Oct 06, 2025 2:00 pm Mine is still doing incredibly well with provider and the fact work pay in a big chunk really helps.

I'm just debating in 12 months time how much of it to take out of the 25% tax free and what to do with it at the time it's not needed etc... In truth most of what i take out will be spent at the time... but i think the rest will go in an ISA unless anyone can tell me otherwise.

The pot after will still be over £500k so i'm not too worried about some spending

Remind me again, this word 'work' you use.....

I'd take option 1Dodgy69 wrote: Fri Oct 31, 2025 7:46 am Received some pension options this week from a company I worked for many years ago for about 6 years. My contributions to this pension was about 6k altogether. Late 80s.

Option 1 is an annual pension of £2822.56

Option 2 is an annual pension of £2075.82 + lump sum of £13833. 00

Option 3 is a transfer value of £55500.00 and put it in my other pot.

Now, we're not talking massive numbers here, but 1 and 2 are guaranteed for life with annual increases in line with whatever. Option 3 goes in the pot and is at risk of the usual market volatility.

Not wanting offical advice here obviously, but which would you choose if it was you, no lump sum required.

The guarantee for life swings it. Sounds like new bike dayDodgy69 wrote: Fri Oct 31, 2025 7:46 am Received some pension options this week from a company I worked for many years ago for about 6 years. My contributions to this pension was about 6k altogether. Late 80s.

Option 1 is an annual pension of £2822.56

Option 2 is an annual pension of £2075.82 + lump sum of £13833. 00

Option 3 is a transfer value of £55500.00 and put it in my other pot.

Now, we're not talking massive numbers here, but 1 and 2 are guaranteed for life with annual increases in line with whatever. Option 3 goes in the pot and is at risk of the usual market volatility.

Not wanting offical advice here obviously, but which would you choose if it was you, no lump sum required.

Draw out and stick in a 5 year ISA at 4.53%. That'll bring in £2,510 a year. A bit less, but it's tax free and you still have the £55,500 safeDodgy69 wrote: Fri Oct 31, 2025 7:46 am Received some pension options this week from a company I worked for many years ago for about 6 years. My contributions to this pension was about 6k altogether. Late 80s.

Option 1 is an annual pension of £2822.56

Option 2 is an annual pension of £2075.82 + lump sum of £13833. 00

Option 3 is a transfer value of £55500.00 and put it in my other pot.

Now, we're not talking massive numbers here, but 1 and 2 are guaranteed for life with annual increases in line with whatever. Option 3 goes in the pot and is at risk of the usual market volatility.

Not wanting offical advice here obviously, but which would you choose if it was you, no lump sum required.

Historically speaking, Stocks and Shares ISAs perform very well. For example, in the past 10 years, the average annual rate of return for Stocks and Shares ISA has been 9.64%.Taipan wrote: Fri Oct 31, 2025 10:53 am I know nothing about investments, how safe are these stocks and shares ISAs?

The value can yo-yo, so if you worry about seeing the value of your portfolio going down then maybe not for you, but invariably there have been few 5-year periods post-war where cash has outperformed the stock market. Also, if think you may need quick access to these funds then doing so during a downturn could cost you money, so best to leave them as a last resort and have alternative investments you can liquidate.Taipan wrote: Fri Oct 31, 2025 10:53 am I know nothing about investments, how safe are these stocks and shares ISAs?

gremlin wrote: Fri Oct 31, 2025 12:27 pmThe value can yo-yo, so if you worry about seeing the value of your portfolio going down then maybe not for you, but invariably there have been few 5-year periods post-war where cash has outperformed the stock market. Also, if think you may need quick access to these funds then doing so during a downturn could cost you money, so best to leave them as a last resort and have alternative investments you can liquidate.Taipan wrote: Fri Oct 31, 2025 10:53 am I know nothing about investments, how safe are these stocks and shares ISAs?

For a very simple way to invest, look at Nutmeg https://www.nutmeg.com/ . Piece of piss to set up, the GUI is dead simple to use. You can set up different 'pots' with different risk profiles to spread your risk.

Just as an indicator, and to prove I put my money where my mouth is, I have two normal savings pots and the remnants of a pension in a pension pot (i.e. subject to rules, etc). One is saving a bit of spends for my upcoming holibobs and that's up 8.28% since July. The other I chucked £500 in a couple of years ago to get the free £50 John Lewis vouchers which is up 30.89% and my pension which has been in since May is up 14.79%.Taipan wrote: Fri Oct 31, 2025 12:39 pmgremlin wrote: Fri Oct 31, 2025 12:27 pmThe value can yo-yo, so if you worry about seeing the value of your portfolio going down then maybe not for you, but invariably there have been few 5-year periods post-war where cash has outperformed the stock market. Also, if think you may need quick access to these funds then doing so during a downturn could cost you money, so best to leave them as a last resort and have alternative investments you can liquidate.Taipan wrote: Fri Oct 31, 2025 10:53 am I know nothing about investments, how safe are these stocks and shares ISAs?

For a very simple way to invest, look at Nutmeg https://www.nutmeg.com/ . Piece of piss to set up, the GUI is dead simple to use. You can set up different 'pots' with different risk profiles to spread your risk.

Nice one, thank you.

in my death , this small pension is reduced even more for spouse, but with the transfer into the pot, Mrs D would get everything.

in my death , this small pension is reduced even more for spouse, but with the transfer into the pot, Mrs D would get everything.